Bruegel Publications Timely measurement of real effective exchange rates Bruegel, Global economy and trade, global governance, trade, trade policy December 23, 2021

report July 24, 2026 Diet session ends with Takaichi on defensive Recess or Reset? Takaichi's Uphill Battle for Public Support and Policy Control... By Tobias Harris Japan Foresight

report July 22, 2026 US Econ | FOMC | GS Mericle Hack David Mericle outlines Goldman Sachs' baseline macro outlook under newly appointed Fed Chairman Kevin Warsh... By Alessio Farhadi

report July 21, 2026 Economic strategy commits Japan to risky course of action State-Led Growth and Security Spending Takes Center Stage... By Tobias Harris Japan Foresight

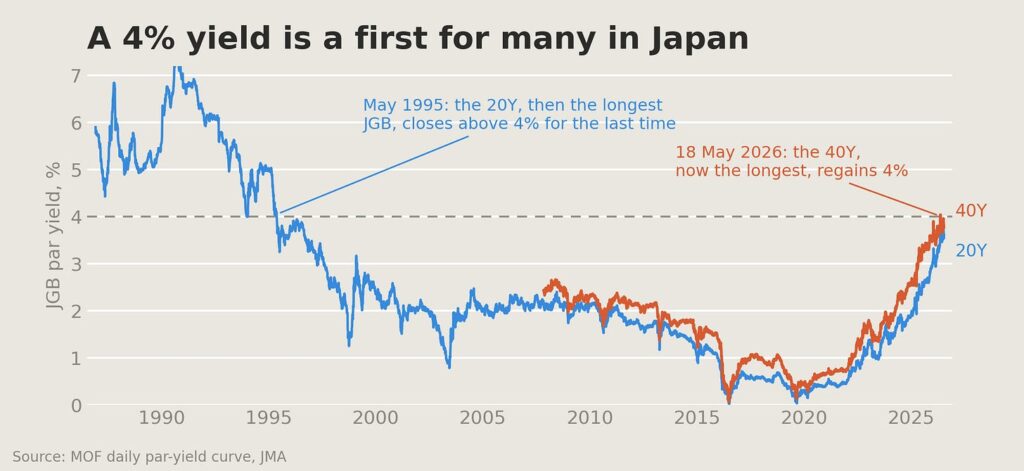

report July 20, 2026 The Long Climb in JGB Yields Is Nearly Over JGB yields saw a historic rise between 2022-2026. Most of the rise came from higher inflation expectations and a normalization of term premia. Our analysis shows the Long Climb is likely nearly over.... By Takuji Okubo Japan Macro Advisors

report July 17, 2026 Yankistan/Eye-Ran/Houthis | Update – July 17, 2026 Who has better intelligence? Brief take on US-Iran escalation... By Alessio Farhadi Speevr Intelligence