Central Bank Research Hub Macroeconomic Changes with Declining Trend Inflation: Complementarity with the Superstar Firm Hypothesis November 22, 2021

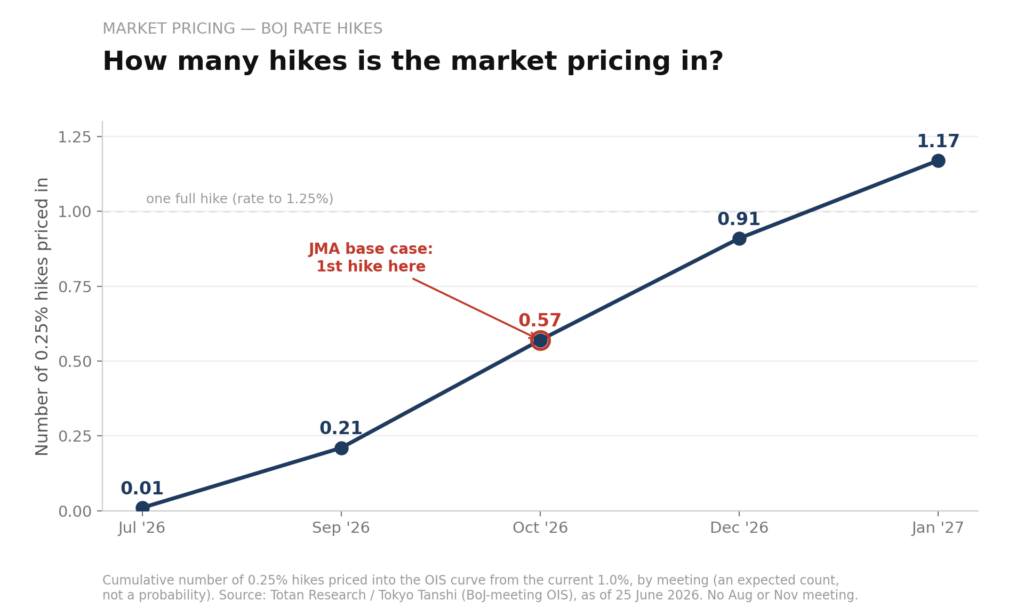

report June 25, 2026 BoJ Steps Up Its Verbal Yen-Intervention The Bank implicitly communicates that defending the yen is now part of its rate hike framework... By Takuji Okubo Japan Macro Advisors

report June 23, 2026 Takaichi presses ahead with tax cut plan despite doubters A High-Stakes Push Against Political Headwinds... By Tobias Harris Japan Foresight

report June 18, 2026 Day 110 | The Islamabad Declaration: What’s in the Deal? 2 versions of 1 MoU — clause-by-clause analysis... By Shahin Iraninejad Global South Strategic Intelligence

report June 16, 2026 No surprises from BOJ as focus turns to fiscal policy Monetary Stability Achieved, Fiscal Challenges Loom for Takaichi Government... By Tobias Harris Japan Foresight

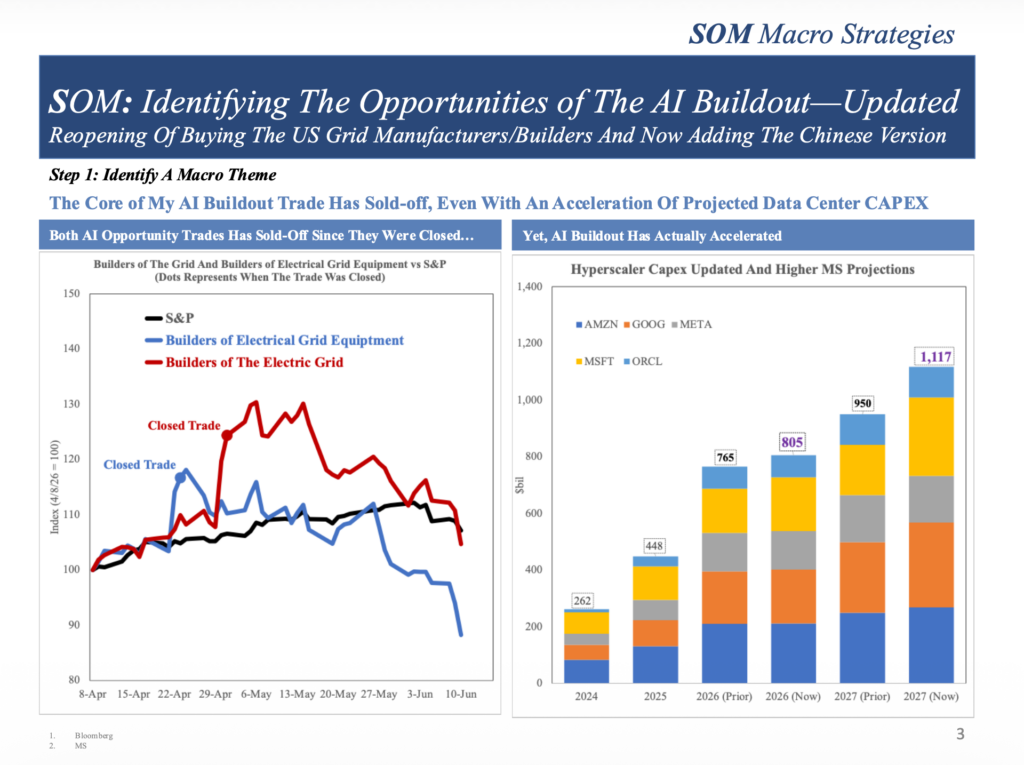

report June 16, 2026 Identifying The Opportunities of The AI Buildout Updated Now Buy US and Chinese Grid Equities... By Alan Brazil SOM Macro Strategies