report May 22, 2026 Government faces new pressures as extra budget proceeds Navigating economic headwinds and political demands... By Tobias Harris Japan Foresight

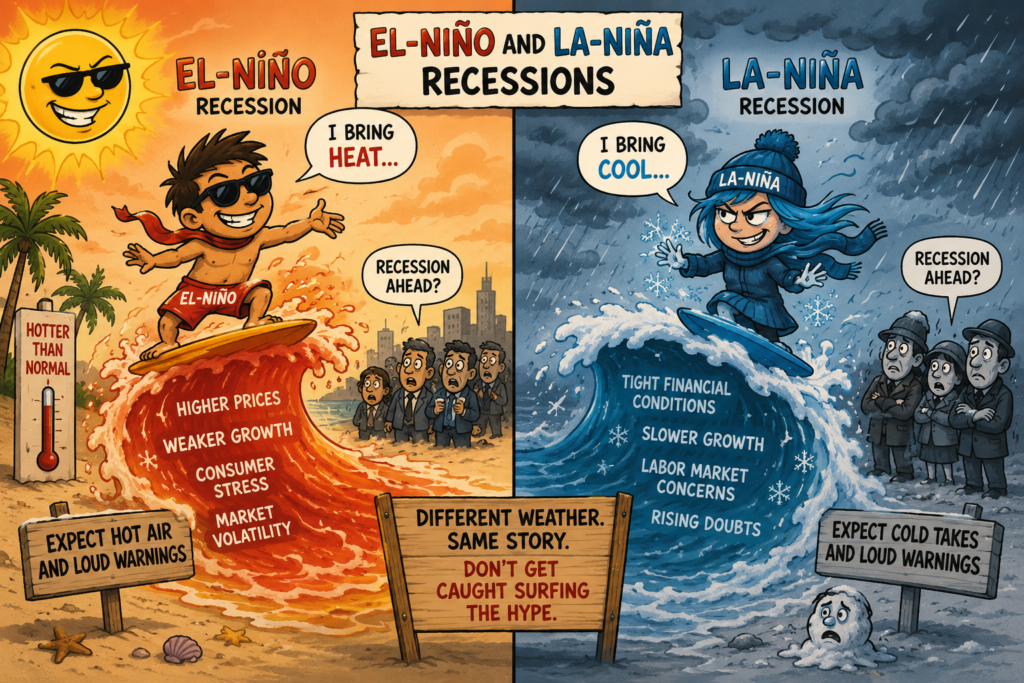

report May 21, 2026 TRADE SIGNAL | U.S. Rates | El-Niño/La-Niña Recessions Summer’s approaching—the annual recessionistas are awakening... By Alessio Farhadi Speevr Intelligence

report May 20, 2026 Japan and South Korea, united in insecurity Navigating regional uncertainty through strategic bilateral cooperation... By Tobias Harris Japan Foresight

report May 20, 2026 China | RMB: Bonnie Glaser & Zongyuan Zoe Liu China's Push to Internationalize the RMB... By Alessio Farhadi Speevr Intelligence

report May 19, 2026 Takaichi pivots on extra budget as crisis impact grows Mounting economic pressures from the Hormuz crisis are forcing a strategic shift in Japan's fiscal and political landscape... By Tobias Harris Japan Foresight