Central Bank Research Hub Passive funds affect prices: evidence from the most ETF-dominated asset classes July 1, 2021

report June 12, 2026 BOJ will send useful signals even with Ueda absent Beyond Ueda: Decoding the BOJ's Next Steps on Rates and Bonds... By Tobias Harris Japan Foresight

report June 10, 2026 Takaichi’s denials do little to stem growing political scandal Defamation allegations, defiant denials, and the rising political cost... By Tobias Harris Japan Foresight

report June 10, 2026 Ex-SIS | Israel: Hebrew Press | Iran | China All politics is domestic — Israel is interesting. Ex-MI6 takes... By Alessio Farhadi Speevr Intelligence

report June 7, 2026 Day 100: Iran Breaks the De-Escalation Trap Missile strikes on Israel in retaliation for Lebanon... By Alessio Farhadi Speevr Intelligence

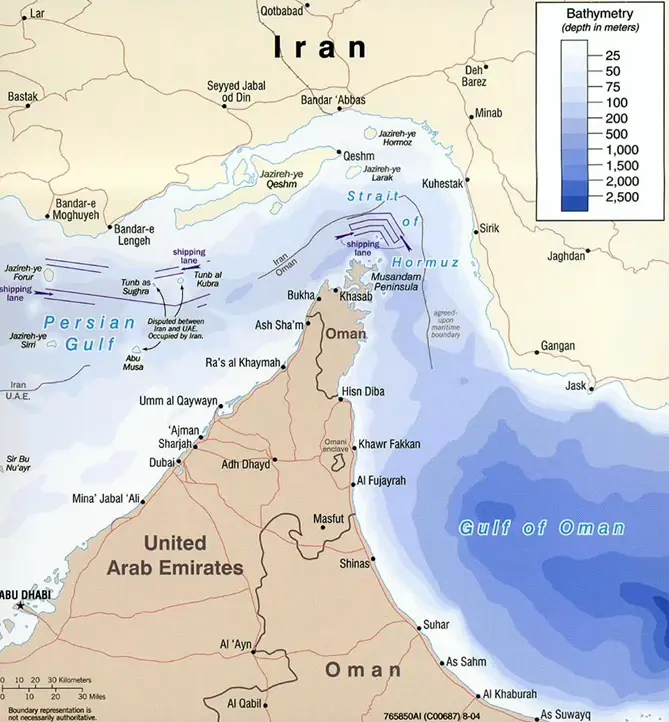

report June 7, 2026 Hormuz: Hostile Takeover?! How a State Built a Governance Framework over a Chokepoint in Sixty-Two Days... By Shahin Iraninejad Global South Strategic Intelligence