report July 1, 2026 Mercy for a Central Bank in a Vice The vice that held the Bank of Japan for four months loosened this morning.... By Takuji Okubo Japan Macro Advisors

report June 30, 2026 The limits of power Ambition Meets Reality: Takaichi's Struggle for Legislative Control... By Tobias Harris Japan Foresight

report June 30, 2026 Spectra Markets | am/FX: USDJPY and NFP Short & to the point today... By Brent Donnelly Spectra Markets

report June 28, 2026 My Recent AI Buildout Opportunity Trades Targets Hit: Cashing Out of the U.S. for China’s AI Boom... By Alan Brazil SOM Macro Strategies

report June 26, 2026 Takaichi’s fiscal gamble comes into view Japan's Ambitious Spending: A High-Stakes Path to Prosperity... By Tobias Harris Japan Foresight

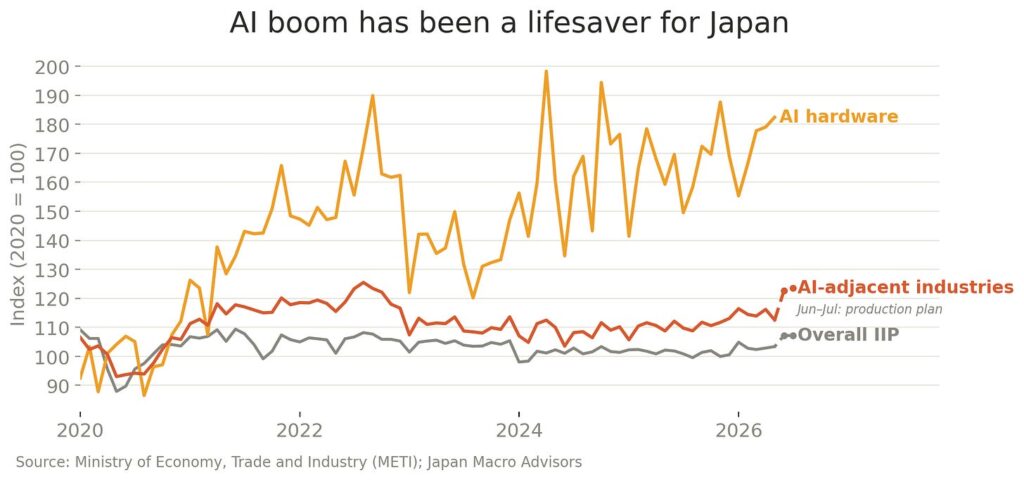

My Recent AI Buildout Opportunity Trades