report June 18, 2026 Day 110 | The Islamabad Declaration: What’s in the Deal? 2 versions of 1 MoU — clause-by-clause analysis... By Shahin Iraninejad Global South Strategic Intelligence

report June 16, 2026 No surprises from BOJ as focus turns to fiscal policy Monetary Stability Achieved, Fiscal Challenges Loom for Takaichi Government... By Tobias Harris Japan Foresight

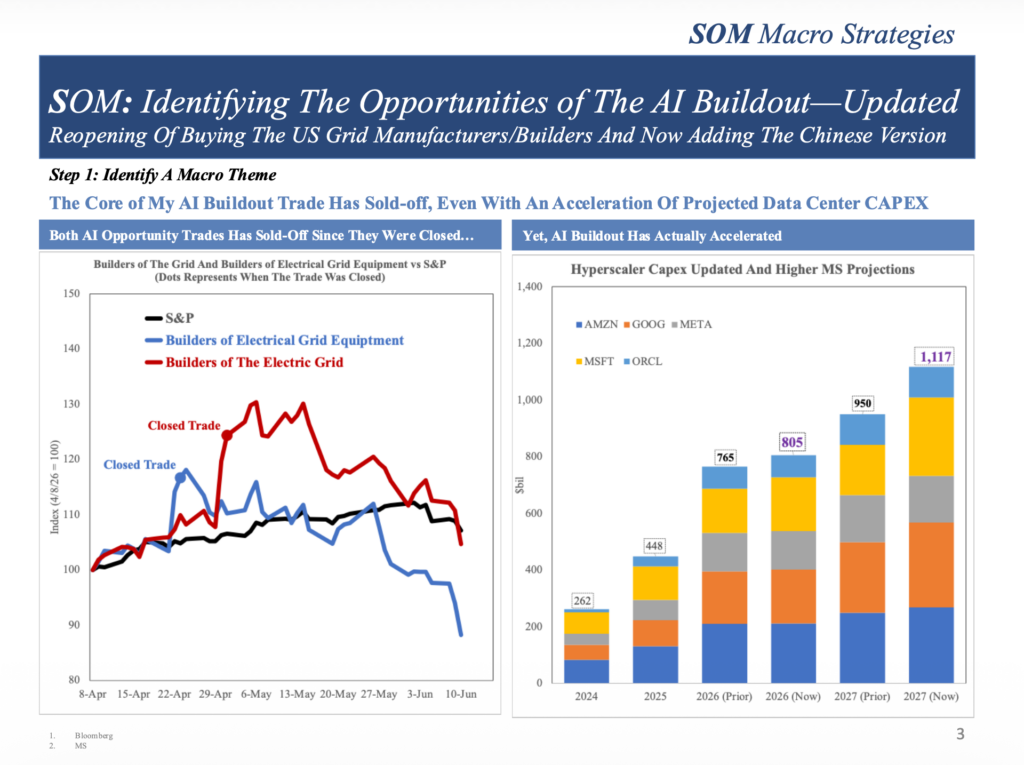

report June 16, 2026 Identifying The Opportunities of The AI Buildout Updated Now Buy US and Chinese Grid Equities... By Alan Brazil SOM Macro Strategies

report June 12, 2026 BOJ will send useful signals even with Ueda absent Beyond Ueda: Decoding the BOJ's Next Steps on Rates and Bonds... By Tobias Harris Japan Foresight

report June 10, 2026 Takaichi’s denials do little to stem growing political scandal Defamation allegations, defiant denials, and the rising political cost... By Tobias Harris Japan Foresight