Is The U.S. Manipulating Oil Prices?

Have you ever met a physical oil trader who isn’t book-smart, street-smart, politically astute, and well-connected? No—me neither.

So we’ll skip the amateur oil-expert commentary and focus on the data.

In recent weeks, there has been considerable speculation around potential manipulation—or even direct market intervention—of oil futures by the U.S. government. As entertaining as that speculation may be, we have seen no credible evidence of direct intervention—only consistent efforts by the White House to talk down oil markets.

The market color we’re hearing (take it with a fistful of salt) is that macro speculators and oil importers have been buying or hedging in futures and forwards markets, while producers in Scandinavia and the Middle East have been selling to lock in current elevated prices.

As a rule, it’s better to side with those actually digging and shipping barrels on the supply side than with paper traders in Manhattan skyscrapers.

The force majeure clause is a whole separate (legal) topic that GSSI has been working on since early this year.

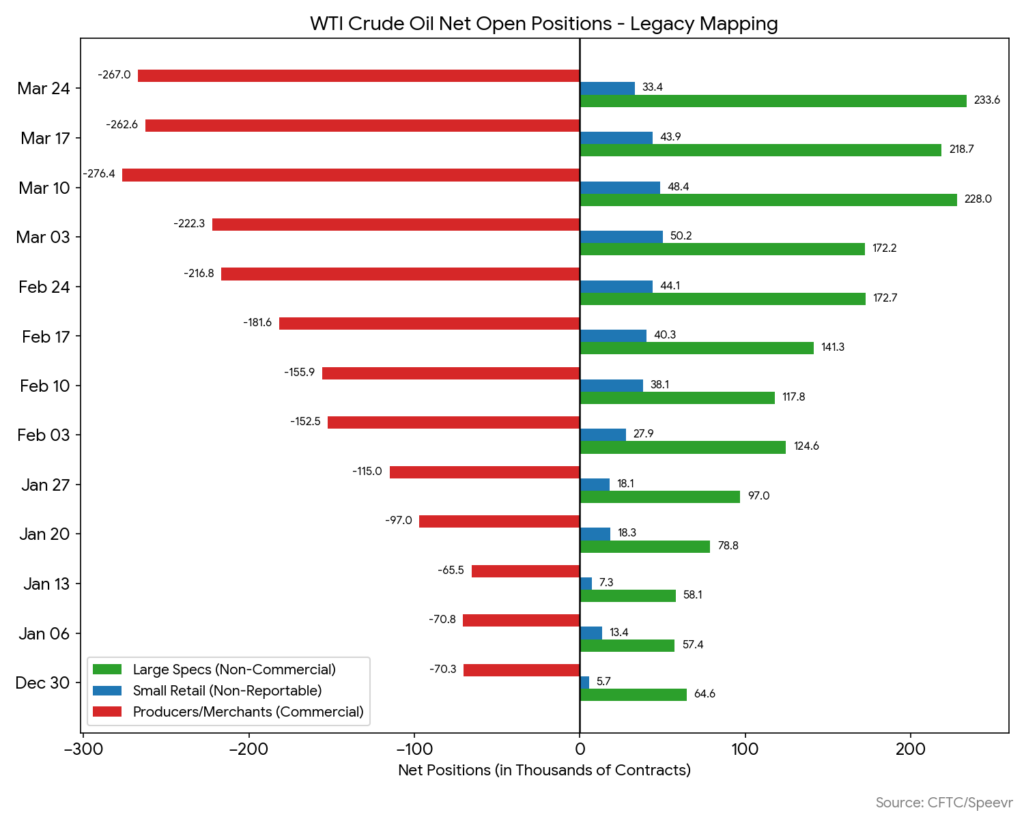

Given the CFTC data below—and a basic understanding of derivatives, with some historical context—it’s possible to piece together a coherent picture of what’s actually going on.

Let's examine WTI crude oil futures first…

Producers stopped adding to shorts/hedges in the second week of March.

Dealers typically carry basis risk, hedging swaps with futures—standard practice. However, the counterparty–market correlation is moving the wrong way, making it increasingly risky to add to positions without raising collateral requirements.

The charts for other petroleum products:

It’s possible the Gulf states are intervening in forward markets at the behest of the White House. However, it’s more likely—and more plausible—that Gulf producers are acting for legitimate commercial reasons, rather than speculating on lower prices.

We would need significantly deeper industry knowledge and market insight to assess the balance between hedging and speculation. Hedging behaviour, much like the oil price itself, is rarely linear and easily predictable.

We can be fairly certain that regulators and bank CVA desks are closely monitoring the risk.