report July 16, 2025 [Spectra | GBP]•[Nvidia | {China, USA}] ⊂ Preeminence Where does real power resides in America?... By Alessio Farhadi Speevr Intelligence

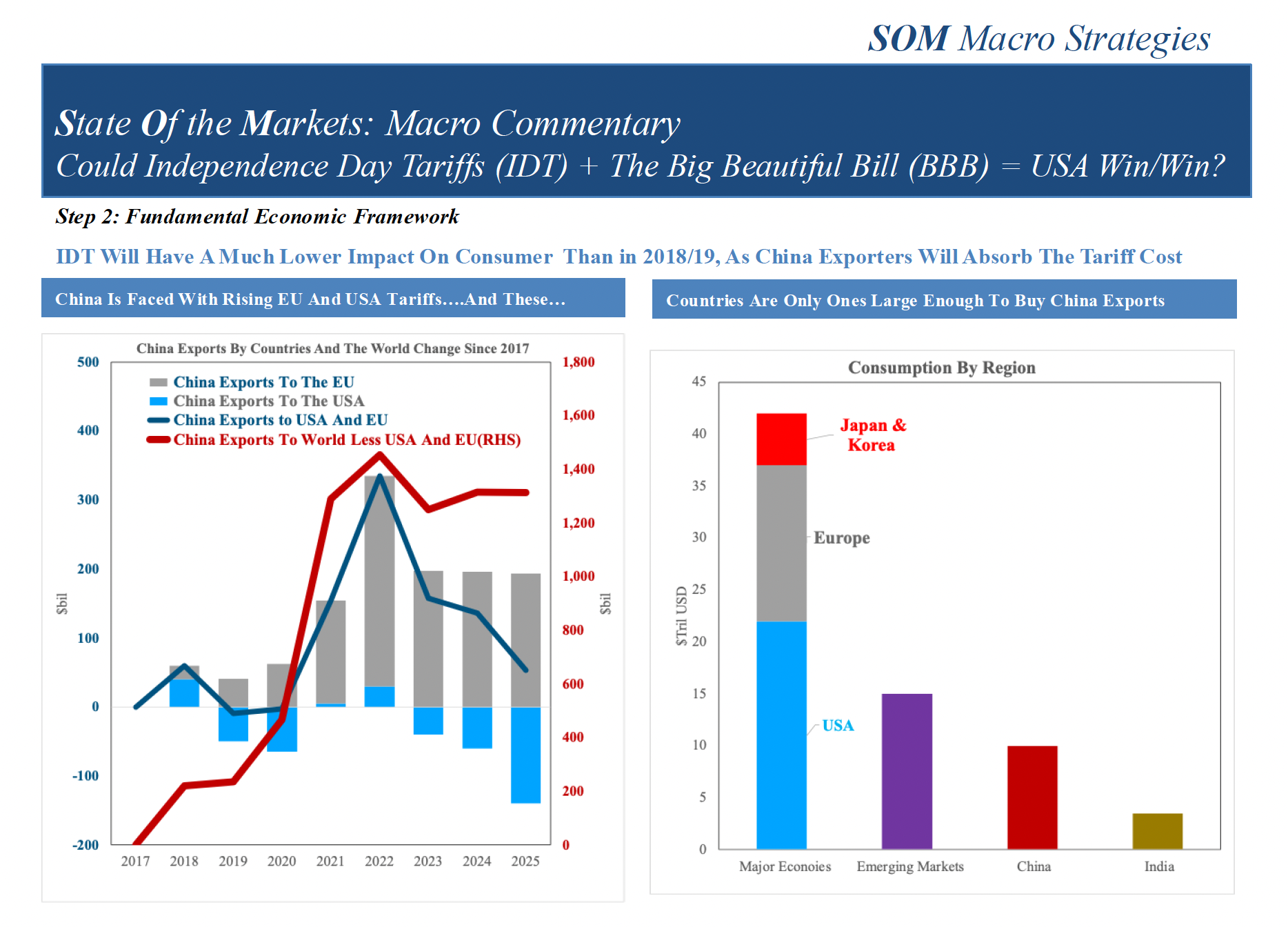

report July 14, 2025 Could Independence Day Tariffs + Big Beautiful Bill Tax Cuts = USA Win/Win Become a member to read the rest of this article Username or E-mail Password Remember Me Forgot Password... By Alan Brazil SOM Macro Strategies

report July 10, 2025 AI | Nvidia | Baupost-Klarman ‘Margin of Safety’ | Boston Bombing From AI to amateur psychoanalysis. We honor the "special ones"... By Alessio Farhadi Speevr Intelligence

report July 7, 2025 London 7/7 | Betting On ‘Bad’ Outcomes Is it ethical or acceptable to bet on disasters?... By Alessio Farhadi Speevr Intelligence

report July 2, 2025 Trump’s Handwritten Note to Powell: Lower Rates Abroad, So Why Not Here? Do lower interest rates in other countries really mean the Fed is too tight?... By Peter Earle Speevr Dialectic